De Blasio’s Executive Order Increases, Expands Living Wage

Amsterdam News - October 9, 2014, by Stephon Johnson - Last week, New York City Mayor Bill de Blasio signed an executive order to increase and expand the living wage to benefit more New Yorkers....

Amsterdam News - October 9, 2014, by Stephon Johnson - Last week, New York City Mayor Bill de Blasio signed an executive order to increase and expand the living wage to benefit more New Yorkers.

At City Hall, while announcing the signing of his executive order, De Blasio said “$13.13 for those without benefits, $11.50 for those who have health insurance and other benefits. This applies to employers, excuse me, employees, I should say, of large groups of employers who do business with the city. Meaning, there’s a lot of companies that do business with the city, that come to the city for subsidies. We think if you want a subsidy, you can prove the need for a subsidy. We want to help you achieve your goals, but we have a standard we hold.”

De Blasio continued, “We need to make sure people are paid a living wage. That’s a fair exchange for that subsidy. What it means—let me put this in real terms—what this means, is the difference between the $8-an-hour minimum wage right now, and the $13.13 that will take effect immediately for those employees of companies that get subsidies going forward. That is a difference of over $10,000 dollars in earnings a year. $10,000. Someone who would have made $16,000—not enough to get by—will now make over $27,000 a year. And that’s a difference maker.”

According to de Blasio, any project that gets more than a million dollars in city subsidies qualifies, stating that it will reach people in lines of work like retail, food services and construction.

Advocates for a raise in the minimum wage have said this action was a long time coming. Shantel Walker, a Papa John’s employee who makes $8.50 an hour and who is a member of Fast Food Forward, praised de Blasio’s actions.

“Nearly two years ago, 200 fast-food workers in New York City walked off our jobs, calling for $15 and union rights,” said Walker in a statement. “Our demand may have sounded crazy at the time, but more and more, $15 is becoming a reality for workers across the country. As we’ve gone on strike again and again and a movement that started here in New York has spread to 150 cities, $15 suddenly doesn’t seem so impossible. From Seattle to Los Angeles to San Francisco and now New York, cities are raising wages so we don’t have to rely on public assistance to support our families.”

Walker also stated that the recent developments are a sign, to her, that minimum wage advocates are on the right side of history.

“While he works with Gov. Cuomo to raise wages for all New Yorkers, Mayor de Blasio’s move today to put workers at city-subsidized projects on a path to $15 is a sign that we are winning,” Walker said. “It’s a step in the right direction and helps push us forward in our fight for $15 for workers across the entire country.”

While the city’s working class has achieved a major victory, the state’s working class is still making the push collectively. Andrew Friedman, co-executive director of the Center for Popular Democracy, pushed for Albany to follow suit in a statement.

“The Albany wage board should eliminate the tipped minimum wage to make this vision a reality and end the wage segregation that traps workers in poverty—workers who are overwhelmingly female and of color,” said Friedman. “Partnering with progressive local, state and federal leadership means we can work together to afford a dignified life for all residents, which means comprehensive policies that include a $15 minimum hourly wage, a predictable and fair workweek, paid sick days and a healthy macro-economy that nurtures equity, creates viable new jobs and protects us from risk-taking by financial institutions.”

Back in the five boroughs, Brooklyn Borough President Eric Adams praised de Blasio for the executive order, citing it as another example of New York City leading the pack. He said that de Blasio had “reaffirmed his commitment to civic innovation and our residents’ welfare by raising the living wage and furthering its reach to thousands more workers. This is a measure that recognizes the cost of living challenges that New Yorkers face and builds a meaningful bridge over the inequality gap we have sought to close across Brooklyn and the rest of the five boroughs.

Source

Turning a Moment into a Movement after the Deaths of Unarmed Black Men

Washington Post - February 19, 2015, by Marc Fisher, Sandya Somashekhar, and Wesley Lowery - In the months following...

Washington Post - February 19, 2015, by Marc Fisher, Sandya Somashekhar, and Wesley Lowery - In the months following the shooting death of Michael Brown, Tony Rice quit his job to lead nightly protests in Ferguson, Mo. But after a grand jury decided in November not to indict the officer who shot Brown, Rice said, “we just woke up one morning and no one was out there protesting.”

That hasn’t deterred Rice. As the nation’s attention has turned elsewhere, he and fellow activists have switched up their tactics, slowing down and digging in, trying to nurture a nascent civil rights movement by shifting to local issues and a broader critique of American society.

The deadly confrontations in Ferguson; in Cleveland, where police shot and killed a 12-year-old boy who was playing with a pellet gun; and in New York, where police choked and killed a man who was selling loose cigarettes on the sidewalk, prompted young people to take to social media and the streets to express outrage and demand change.

The unrest generated by the deaths of Brown in Ferguson, Tamir Rice in Cleveland and Eric Garner in Staten Island may eventually become the first scene in a stirring saga of how a moment builds into a movement. Or it could end up as a cautionary tale about how a righteous activism born of traumatic incidents fizzles, the energy of dozens of new activist groups sapped by quotidian realities and the shortened attention spans of a society that expresses its political passions in Likes and tweets.

“To go from protesting to power, you need demonstrations, legislation and litigation,” said the Rev. Jesse Jackson, the veteran civil rights leader who has acted in recent months as an informal adviser and cheerleader for several new groups. “Sprinters burn out real fast. These young people need to be in it for the long run. And it must be an intergenerational coalition. A movement that’s mature requires clergy and lawyers and legislators. The struggle is never a one-string guitar.”

The new activists are still trying to tune their instrument. They are still figuring out whether to hew to local issues or go national. For the most part, the young protesters haven’t connected with elders such as Jackson or the Rev. Al Sharpton. They have uneasy relationships not only with civil rights fighters of generations past, but also with the black mayors and police chiefs who owe their own positions to the successes of that earlier activism.

All that adds up to a fractured puzzle composed of idealistic young activists who believe ordinary people can band together to make black lives matter more, but who haven’t yet figured out how to boost their generation into action.

In Ferguson, some activists moved from street actions to events such as “Books and Breakfast,” a giveaway featuring books such as “The New Jim Crow” and “I Love My Hair!” and free yogurt parfaits. One recent day, only a few dozen people stopped by, mostly familiar faces of hard-core activists.

Nonetheless, they talked about marching at a local high school where white students had said disparaging things about black protesters. The meeting ended with pleas from organizers to hug someone in the room and take another look at the books, half of which were left unclaimed.

Two days before the book event in Ferguson, the roads were slick in Cleveland, with heavy snow falling, as about a dozen activists gathered at the Unitarian Universalist Society in Cleveland Heights — a racially and economically mixed suburb up the hill from downtown.

The meeting, called by a local activist group called Puncture the Silence, was an effort to press beyond the squabbles and rivalries that have plagued the protest groups that emerged after the Rice shooting. Although protests have continued almost weekly in Cleveland through a harsh winter, the wait to hear whether the officers involved in the shooting will face criminal charges has left many activists frustrated, splintered by arguments over strategy, objectives and media posture.

Some want more marches, sit-ins and disruptive protests. Others propose to stage a tribunal, rendering an extrajudicial verdict in several cases of police use of force. Still others want a focus on policy, but what should they demand? Body cameras? Special prosecutors? Police training? Collective bargaining?

“We need to keep the direct pressure on elected officials, but we also need to stay active in the streets,” Rachelle Smith, 31, who has been a key player among Cleveland’s young protest groups since the Rice shooting, told the group.

The next move after expressing anger in the street is often the hard part for new civil rights groups. Do they seek changes in the law? Push to elect sympathetic candidates? Focus on winning over those who aren’t yet on their side? Or pull back from the moment and get radical, pressing for wholesale social change?

In Ferguson, many of the more than a dozen organizations that formed in the tear-gas clouds of August fragmented over the course of the fall. Conflicts flared over organizers who spent much of their time honing their profile on Twitter and attending an endless series of conferences on activism. Members of some new groups grumbled about leaders who seemed more interested in scoring airtime with Don Lemon on CNN or winning donations from wealthy celebrities than about recruiting poor people to their cause.

On the night of the grand jury’s decision not to indict Officer Darren Wilson in the Brown shooting, Tory Russell and other members of a new civil rights group called Hands Up United knew one thing they had to do: Race to their office to fend off vandals and prevent violence.

Today, six buildings across from the group’s original office remain boarded up. The Metro PCS shop is a blackened heap; a steel bar bears a slogan written in rust: “America Wake Up!”

Hands Up United has moved to a new location but isn’t going away, said Russell, a burly man with a thick beard who wears his devotion to the movement on a T-shirt emblazoned with the first names of young African Americans whose deaths have fueled this fight — Trayvon, Mike, Eric . . .

By the time Brown was killed, Russell, 30, had already dropped his plan to become a teacher — a dream he traces to his days in the library at Sumner High School in St. Louis, alma mater of Chuck Berry and Tina Turner. Today, Russell views his old school as dominated more by in-school suspension than reading books, so he has focused his political work on distributing books on black history and radical politics.

He sees a surer path to change at the neighborhood level than in any effort to win nationwide notice. “And now the real work begins,” Russell said. “You can complain about the system being bad and how it affects the community. But if your room is dirty, you’re going to have to pick up the clothes and wash the dishes. And that’s what we’re doing.”

Hands Up’s leaders haven’t lost sight of the issue of police brutality: “We still believe the ultimate piece of the narrative is that unarmed people are being killed by police,” said Tef Poe, 27, a rapper from St. Louis who started the group with Russell.

But since the TV cameras left town, the heady camaraderie of those first weeks has given way to infighting and a struggle for attention.

Poe joined other organizers on a trip to the Palestinian territories last year and he recently returned from the Sundance Film Festival — decisions that have raised questions among some activists about how groups are spending the hundreds of thousands of dollars that have come in from foundations and ordinary people who hit “donate” buttons online.

Poe and Russell said they are not getting paid by Hands Up. Neither was sure of the exact size of the organization’s budget. Hands Up United — which like many of the new groups has not established nonprofit status of its own — has received organizational help from a group connected with the California antiwar nonprofit known as Code Pink.

Russell said Hands Up United, unlike other groups that flared on TV and Twitter and then disappeared, is in it for the long run. “For some people, when it wasn’t sexy anymore, when CNN left, it died down for them,” he said. “What we’re doing is not hashtag activism, this is actually community organizing. I’ve never seen hashtags change my community.”

Athousand miles away, Hands Up United’s shift in focus from civil disobedience to community development — from leading rallies to giving out books — sounds familiar to Phillip Agnew.

The group he founded in 2012 — after a former neighborhood watch volunteer shot and killed Trayvon Martin, an unarmed black 17-year-old in Sanford, Fla. — had a two-year head start on those that have emerged in Ferguson and Cleveland. Agnew’s Dream Defenders have been through it all: the rush of the marches, a 31-day sit-in in the state capitol, confrontations with the powerful, promises that they would be listened to, frustration when nothing changed.

Now, on the same day that Hands Up United gives out books in Ferguson, Agnew’s Dream Defenders stage a multicultural festival in front of a sprawling, brightly colored mural of Haitian village life in Miami’s Little Haiti neighborhood. The attractions includesalsa dancing and African drumming; speeches in English, Spanish and Creole; testimonials from farmworkers and college students — all spiced with gentle reminders of the need to do something about the number of young people from Miami’s crazy quilt of impoverished communities who drop out of school, land in prison, or subsist without career or much hope of one.

The Dream Defenders — the name refers to the effort to build on the Rev. Martin Luther King Jr.’s legacy — started out demanding the repeal of Florida’s “stand your ground” law, which allows people to use deadly force if they feel threatened by another person. But after their sit-in failed to persuade Gov. Rick Scott (R) to call a special session of the legislature to reconsider the law, Agnew and his fellow Defenders concluded that they needed to move on to “the next phase.”

What that would look like took many months to decide. Agnew — at 29, he is thoughtful yet blunt, insisting on talking about fomenting revolution even when his older advisers counsel more moderate rhetoric — said he was initially distracted by the celebrity that came with being a prominent activist.

“It was very easy to accept invitations all over the country,” he said. “It’s very, very, very alluring and seductive to have folks know you and to go to conferences and workshops every week. I was in Time magazine, on television all the time — it does begin to create some kind of friction within the organization. And then you look up and feel like we haven’t gotten anywhere. We had to pump the brakes.”

Some other groups that formed after Martin was killed have left Florida and are trying to find traction on a nationwide scale. The Million Hoodies Movement for Justice was started by a young Floridian, but its leaders are now spread around the country, active mainly through video and social media.

“Nobody’s going to have their political beliefs changed on Facebook, but it is a way for us to connect,” said Peter Haviland-Eduah, the group’s spokesman, who lives in Michigan, where he is in graduate school. “We want to build coalitions across the country, and we have to find small, tangible wins. The civil rights movement in the ’60s was about changing laws and they had tangible goals, like getting more folks to register to vote. We’re about changing the consensus, changing beliefs, and that’s much more difficult.”

The Dream Defenders concluded that the only way forward is to embed themselves in local issues. “It’s a big mistake for these groups in Ferguson and other places to go national,” said Sherika Shaw, 26, the group’s South Florida coordinator, who left a graduate program in art education after learning about Dream Defenders on Instagram. “The people are here, where you are. It’s not about changing policy; you can’t use the master’s tools to destroy the master’s house. We don’t want to be the people the TV networks call; we want to be who the people call instead of the police when there’s a domestic dispute.”

Shaw spends her days trying to establish Dream Defenders groups in local high schools, appealing to teens to speak out against having uniformed security officers on their campuses.

The group’s core members lived for a time in a borrowed house in the lush suburb of Miami Lakes — the dream house, they called it — allowing them to talk and plan around the clock. They lived on Agnew’s credit card and his savings from four years he spent selling erectile-dysfunction and anti-depression drugs for a pharmaceutical company in North Carolina.

They studied past movements, read history and made two defining decisions: Unlike many other new groups, they would stay local, rooting themselves in Florida’s problems and people. And they would get radical, spurning elective politics and emphasizing their belief that the persistent poverty and social immobility in many black communities result not from specific policies but from the very nature of capitalism and racism.

On one morning in early February, Agnew arrived at work angry because he woke up to a flat tire on his car. “This system of capitalism creates a lot of stress around money,” he said. He put on his black “People Over Money” T-shirt and began another day of trying to convince blacks and Hispanics that the problem they see as police brutality is really far deeper.

“A community that just lost someone to a police shooting may not be ready to hear that,” he said. “They may not have that language. But if we talk to them about what they experience — being ignored, being invisible, the contempt for black people, the contempt for poor people — they begin to see that this is much larger.”

At the street festival, which draws about 150 people over the course of the afternoon, Shamile Louis, the 23-year-old daughter of Haitian immigrants, tries to get that message across. Louis, who has worked with Dream Defenders since her junior year in college, recalls watching George Zimmerman’s trial in Martin’s shooting on TV every day; when he was acquitted, “my soul was shattered,” she said. She spent 27 days at the sit-in at the capitol in Tallahassee. But although she’s still committed to the cause, the realities of surviving are pulling her away from full-time activism.

“I’m going to have to find work,” she said. “The movement is really struggling. We were really amped up at the capitol. The reality now is people have real lives and have to work.”

She spent part of the afternoon at the Dream Defenders table in the center of the courtyard. By day’s end, only six people have signed cards expressing interest in the group’s work.

Jesse Jackson came to Tallahassee to join the Dream Defenders in their sit-in. Sharpton shuttled into Ferguson to lead marches and rustle up media attention. Black clergy and leaders of traditional civil rights groups reached out to the new groups, offering advice and organizational support.

And in December, Agnew and six other leaders of new groups met at the White House with President Obama, who told them he would set up a task force to address the “simmering distrust” between police and African Americans. Agnew came away from the meeting convinced that protest groups must become more radical because change will not come from those already in power.

“The concessions won by the civil rights movement in the ’60s are our biggest obstacle,” he said. “We have black Fortune 500 CEOs, an African American president, African American mayors and chiefs of police, and still the lot of black people, Latino people, has not risen.”

Dream Defenders, which has a minimally paid staff of seven, works largely off a $200,000 grant from the Tides Center, a San Francisco-based foundation that supports groups seeking social change. Agnew said he expects the Tides money to dry up eventually “because in the end, we’re going to be too radical for them.”

In Cleveland, the mayor, police chief and much of the City Council are black, as are many influential pastors. But some young black activists say their fight puts them squarely at odds with the city’s black power structure.

“As an African American guy trying to make a difference, I am fighting the white establishment, and I’m also fighting the black establishment,” said Alonzo Mitchell, an organizer who hosts a local radio show and is a regular at council meetings.

When Mitchell, 33, approached a city official to seek backing for a mentorship program for future political leaders, he says he was told: “No one is going to teach you. Power is never given, it’s taken.”

On the city’s west side, below the modest Guide to Kulchur bookstore, an expansive basement meeting room has become the headquarters of an activist collective determined to change how Cleveland police operate.

In the basement one recent afternoon, activists peppered half a dozen council members with demands, insisting that each official complete a report card, answering yes or no to statements such as “The officer who killed Rice should be immediately indicted.” All but one of the council members in attendance said they favored an indictment.

When protesters planned a march after the Rice shooting, Police Chief Calvin Williams volunteered to shut down parts of a highway. Commuters griped about the protests impeding traffic, but Mayor Frank Jackson said “that’s the inconvenience of freedom.” Cleveland police officers working at demonstrations conversed and joked with protesters, a strikingly different approach from officers in St. Louis, who met similar protests with riot gear, tear gas and rubber-coated bullets.

Despite such efforts at cooperation, pressing for change is harder in cities with black elected officials, some veteran civil rights leaders say.

“It is more difficult to organize against a black power structure,” said Lawrence Hamm, 61, who formed the People’s Organization for Progress in Newark in 1983 after a police shooting of an unarmed black man. “You might be marching against a popular black mayor, and it’s going to be harder for you to get people to join you.”

The new groups need help from the old-line black civil rights groups they sometimes view as having sold out, Hamm said: “The black radical organizations — the people who want more fundamental change — are not going to be strong enough to get there on their own.”

Although Hamm’s group still agitates for police overhauls, its founder long ago realized he needed to work both with elected officials and with older, mainstream organizations.

“We formed our group because we felt the traditional civil rights groups were not aggressive enough,” said Hamm. “But now, I belong to three branches of the NAACP.”

Three decades after Hamm set out to be more in-your-face than the black organizations of his parents’ generation, Ciara Taylor, the 25-year-old political director of Dream Defenders, found her way to a more radical path by volunteering in Obama’s 2008 campaign.

Knocking on doors in Vero Beach, Fla., she was called the n-word and confronted with the reality that a black senator’s candidacy for president “does not make race go away,” she said. “There was a great hope within my generation and within me that we could be free of racial identification, but we realized that race does not go away.”

But it took a one-two punch three years later to propel her into full-time activism: In her senior year at Florida A&M University, the school proposed to eliminate her major, Spanish language; she switched her concentration to political science and joined a campaign to reverse the cutbacks. A few months after that, when Martin was killed, Taylor, daughter of a corporate manager and a career Navy officer, felt jolted from her middle-class trajectory.

“Being a young person, you’re impatient,” she said. “You see these trigger moments happen and you automatically want to fight the big beast that our parents tried to protect us from.”

Now, two years into her life as an organizer, Taylor bristles at the notion, expressed by some veterans of the 1960s movement, that the new activism is dissipating. “A lot of the older generation looks at movement work as physically being at a protest,” she said. “That’s important, but a more radical expression of social engagement is simply choosing to love yourself in a society that tells you you look like a thug or your nose is too big.”

When Taylor sees new groups fading away, she doesn’t take that as a defeat, but as a sign that people are “caring for themselves. The fact that a lot of movements are disintegrating comes from the inability to care for oneself, especially mothers with families.”

Ferguson remains a hive of activism. For the first time, the Organization for Black Struggle, which grew out of the Black Power movement of the 1970s and ’80s, has enough money to pay six staff members, thanks to support from individuals and progressive groups such as the Center for Popular Democracy, Color of Change and the Open Society Foundations, which was founded by liberal billionaire investor George Soros.

Seven months ago, Charles Wade was adjusting scarves and trimming hems for Hollywood stars. Now he’s in St. Louis, where the former image consultant to Solange Knowles, Beyoncé’s sister, is alone, in black sweats, scrubbing the floor of a townhouse that is part of a transitional housing program he has set up through his new organization, Operation Help or Hush.

It’s been a trying few days. His asthma was acting up. A protester he’s been housing lost Wade’s credit card while out buying supplies. And on Twitter, he’s dealing with a protester who questioned his funding, his newfound fame as an activist and his devotion to the cause.

“It’s really demoralizing that you have to fight so hard just to do something decent for people,” Wade said.

Immediately after the Brown shooting, Wade, a native of Bowie, Md., started raising money on Twitter to provide food, housing and even expense money for protesters who paused their lives to go into the streets. He raised $25,000 in one week. On one occasion, after putting out a call on Twitter for help for protesters who needed gas money, Wade stood in the parking lot of Andy Wurm Tire & Wheel handing out $20 bills.

Since grand jurors decided not to indict Wilson, many activists have scattered. Wade stayed. He still expects to house 27 new activists by April, and he’s raising money through Twitter and from friends and family.

He’s determined to keep going, he said; there’s so much more to do: “There’s very little we’ve actually gotten for Ferguson except for it to be known nationally.”

Source

The Federal Reserve Should Not Increase Interest Rates

Later this month, the world's top financial and economic policymakers will pow-wow at the Federal Reserve Bank annual meeting in Jackson Hole to determine whether it is time for the Fed to roll...

Later this month, the world's top financial and economic policymakers will pow-wow at the Federal Reserve Bank annual meeting in Jackson Hole to determine whether it is time for the Fed to roll back recession-era policies -- e.g. a near-zero benchmark interest rate -- put in place to support job growth and recovery.

This would be the wrong decision for the communities that are still struggling to recover and the wrong decision for America. Advocates for higher interest rates point to an improving job market as a sign that America has come back from the recession. But many activists, economists, and community groups know that raising interest rates now would stymie the many communities, particularly those of color, that continue to face persistent unemployment, underemployment, and stagnant wages. As the Fed Up campaign, headed by the Center for Popular Democracy, notes in areport released this week, tackling the crisis of employment in this country is a powerful and necessary step toward building an economic recovery that reaches all Americans -- and ultimately, toward building a stronger economy for everyone.

The report, "Full Employment for All: The Social and Economic Benefits of Race and Gender Equity in Employment," shares a new data analysis by PolicyLink and the Program for Environmental and Regional Equity (PERE) estimating the boost to the economy that full employment -- defined as an unemployment rate of 4 percent for all communities and demographics along with increases in labor force participation -- would provide. While overall unemployment is down to 5.3 percent, it is still 9.1 percent for blacks and 6.8 percent for Latinos. Underemployment and stagnant wages have further driven income inequality and hinder the success of local economies. By keeping interest rates low, the Fed can promote continued job creation that leads to tighter labor markets, higher wages, less discrimination, and better job opportunities -- especially within those communities still struggling post-recession.

Lowering unemployment to 4 percent for all gender and racial groups (the rate of overall unemployment in 2000 when the economy was last at full employment) and increasing labor force participation rates would mean that 14.3 million more Americans are employed, 9.3 million fewer would live in poverty, GDP would increase by $1.3 trillion, and the government would receive an additional $261 billion in tax revenue, according to the report.

Full employment would also have an enormous positive impact on racial inequities in income. Currently, only half of workers of color make at least a living wage ($15/hour), compared to 69 percent of white workers, and median household income within communities of color is significantly lower compared to white households. With full employment, black households would see their incomes rise 23 percent, Latino households would see a 14 percent increase, and Native American households would see a 32 percent increase.

Armed with this data, which was compiled as part of ongoing economic research by PolicyLink and PERE's National Equity Atlas team, Fed Up will host its own meeting in Jackson Hole, featuring presentations by this team, activists, economists, and community organizers. This meeting, concurrent with the Fed's, aims to put pressure on the Federal Reserve to acknowledge those communities of color still mired in the recession and take up policies that will bring full employment to all. While Federal Reserve policies are not the only solution to boosting employment among those communities so often left behind, they are a vital and necessary step towards building a stronger, more inclusive American economy.

Source: Huffington Post Politics

Organize Florida activists protest Trump infrastructure plan

Progressive activists gathered on the shores of Lake Parker on Thursday to air their discontent with the Trump administration’s outline for a nationwide infrastructure improvement plan.

The...

Progressive activists gathered on the shores of Lake Parker on Thursday to air their discontent with the Trump administration’s outline for a nationwide infrastructure improvement plan.

The plan, outlined broadly in a six-page memo released last month, amounts to placing heavy burdens on the poor through flat user fees like tolls, subsidizing private companies and ignoring public transportation, school facilities and clean energy, said activists with Organize Florida, a project of the Center for Popular Democracy, a left-leaning political advocacy group.

Read the full article here.

How Janet Yellen Is Embracing The Fed’s Role In Racial Justice

How Janet Yellen Is Embracing The Fed’s Role In Racial Justice

Oh, what a difference a year can make.

Last July, Federal Reserve chairwoman Janet Yellen endured criticism for House testimony in which she seemed to imply that there was little the Fed...

Oh, what a difference a year can make.

Last July, Federal Reserve chairwoman Janet Yellen endured criticism for House testimony in which she seemed to imply that there was little the Fed could do to address the disproportionately high African-American unemployment rate.

Not so on Tuesday. In her semi-annual testimony to the Senate Banking Committee, Yellen emphasized that the failure of the economic recovery to reach communities of color influences the Fed’s decision-making, and made a strong commitment to improving diversity at the central bank.

“Jobless rates have declined for all major demographic groups, including for African Americans and Hispanics,” Yellen said, according to her prepared remarks. “Despite these declines, however, it is troubling that unemployment rates for these minority groups remain higher than for the nation overall, and that the annual income of the median African-American household is still well below the median income of other U.S. households.”

Yellen’s policy argument has not fundamentally changed. It is the Fed’s job to maximize employment in the economy as the whole, she says, and it lacks the tools to target particular communities. And the Fed chief has clarified since last summer that she takes seriously how the Fed’s adjustment of interest rates can have an especially big impact on African Americans and Latinos, who have higher jobless rates.

But Yellen’s remarks and actions on Tuesday represent the Fed’s greatest demonstration yet that it is putting the concerns of communities of color front and center on its agenda.

The Fed Up campaign, a coalition of progressive groups that has led the push to make the Federal Reserve more responsive to workers in general, and communities of color in particular, was pleased with the focus of Yellen’s testimony.

“Each time since Yellen spoke last July, when she got pushback over what she said, she has gotten a little bit better,” said Jordan Haedtler, Fed Up’s campaign manager. “Now she is proactively showing that the Fed is assessing this data and does take this data into account.”

Diversity is an extremely important goal and I will do everything I can to further advance it.

This week’s hearings, held every six months in both chambers of Congress — the House will hold its hearing on Wednesday — are an opportunity for the Fed chair to update lawmakers about the overall state of the economy. As part of the briefing, the Fed releases an accompanying monetary policy report summarizing its economic assessment and research.

For the first time, the Fed chose to devote a section of its report to whether the “gains of the economic expansion [have] been widely shared.” That section focused on how the recovery affected different races and ethnicities differently.

The results are discouraging. Despite years of job growth, the rates of full-time work for African Americans and Latinos are a few percentage points lower than they were before the recession, while the rates among white and Asian-American workers have more or less reached pre-recession levels. And the median income of black households, which took the biggest hit of any group during the recession, has also been slower to recover, reaching only 88 percent of what it was in 2007, compared with about 94 percent for the other three groups.

Responding to a question about the new section from Sen. Sherrod Brown (D-Ohio), Yellen insisted that weighing the disparate impact of economic growth on a range of different groups is a key part of the Fed’s mission.

“There are very significant differences in success in the labor market across demographic groups,” she said. “It is important for us to be aware of those differences and to focus on them as we think about monetary policy and the broader work that the Federal Reserve does in the area of community development and trying to make sure that financial services are widely available to those that need it, including low- and moderate-income [households].”

Yellen also recognized the importance of diversity — of race, gender, professional background and ideology — within the Fed’s ranks in ensuring the bank remains sensitive to a broad array of Americans’ economic experiences.

She touted her creation of a task force in the Fed to improve its gender and ethnic diversity, but acknowledged there is more to be done.

“Diversity is an extremely important goal and I will do everything I can to further advance it,” Yellen said.

Progressive groups and their allies in Congress trying to make the Fed more accountable to the public have focused on increasing diversity and reducing Wall Street’s influence at the central bank. Eleven senators, including Elizabeth Warren (D-Mass.) and Bernie Sanders (I-Vt.), and 116 House members sent a letter to Yellen on May 12 urging her to prioritize the diversity of Fed officials, especially at the 12 regional Fed banks, which are privately owned. (Hillary Clinton expressed similar sentiments in a statement later that day.)

The makeup of the regional Fed bank boards is important because they are dominated by the big banks and have free reign to appoint their presidents. The regional Fed bank presidents hold five seats on the Federal Open Market Committee, the central bank panel that adjusts the benchmark interest rate. Currently, regional Fed presidents make up half of the FOMC’s influential votes.

As a result, the Fed officials with the power to raise interest rates and effectively increase unemployment are selected by people who are disproportionately white, male and from the finance and business sectors.

In the interests of changing that, the Fed Up campaign on Monday released a slate of 39 candidates for the regional Federal Reserve bank boards of directors. The candidates not only reflect racial and gender diversity, but also come exclusively from academic institutions, community groups and labor organizations.

“On racial and gender diversity there has been modest progress, though it has not taken place at the rate we would like to see,” Haedtler said. Haedtler added that there is even greater room for improvement when it comes to the diversity of professional backgrounds of board members and other top Fed officials, an area where he said there has been “regression” under Yellen’s watch.

By Daniel Marans

Source

Report: Threat of Foreclosure on Calif. Homes Disproportionately Affects Minorities

National Journal, The Next America - March 15, 2013 - Leading mortgage lender Wells Fargo is urged to be more transparent about relief reporting and to grant principal reductions. An overwhelming...

National Journal, The Next America - March 15, 2013 - Leading mortgage lender Wells Fargo is urged to be more transparent about relief reporting and to grant principal reductions. An overwhelming majority of homes in California’s major cities that are in danger of foreclosure are also in majority-minority ZIP codes, according to a report released this week.

The report focuses particularly on homes with mortgages serviced by Wells Fargo. Of the 21 major California cities examined, more than eight in 10 homes in danger of foreclosure are in areas where at least half of its residents are minorities—evidence, the report’s authors say, that further supports the idea that the housing crisis has been particularly harmful to African-American and Hispanic homeowners.

The findings come on the heels of the housing-market decline and the ensuing Great Recession that ensnared many homeowners who have been fighting to maintain their financial standing and retain their homes. While the report focuses on the California economy, other Americans are in similar circumstances. Across the nation, homeowners—many of them minorities—struggle to stay afloat as they watch their savings plummet and their dreams of maintaining a middle-class American lifestyle disappear. In its place are notices of default and the impending threat of bankruptcy.

In California, a total of 65,466 homes are in the pipeline for foreclosure, many of them purchased before the housing market crash in 2007.

Coauthor Ady Barkan, of the Center for Popular Democracy, a national organization based in New York, said the report focuses on Wells Fargo because the bank is responsible for the highest number of homes in California’s foreclosure pipeline—in addition to being headquartered in the same state. As leading lender, the bank is responsible for mortgages for 11,616 California homes—nearly 1 in 5 homes in the pipeline.

The “foreclosure pipeline” refers to homes that have received a notice of default or a notice of trustee sale. While some homeowners eventually pay back the debt, more often the homes are foreclosed, Barkan said.

Wells Fargo spokeswoman Vickie Adams took a contrary view, saying that the term “pipeline” can be overused and doesn’t take into consideration the complexities of the mortgage-lending industry. She added that the bank offers various programs and workshops to help educate its customers on their options to prevent losing their home.

“It’s always challenging to articulate some of the specifics of what some perceive to be a pipeline of sorts,” she said. “The facts are when a home has come to foreclosure, there are oftentimes that a customer is able to find options to prevent [it].… In foreclosure, no one wins. What we do is try to provide a great deal of support to the community in a number of ways.”

The wide variety of data sources that reports use can often create conclusions that aren’t necessarily in line with standard industry practices, Adams added.

“We all understand everyone’s right to raise issues they believe are important, but I think it’s really important, again, to look at the data and understand what the data says and use the measures that are appropriate for the industry,” she added.

According to the report, the opaque nature of Wells Fargo’s reporting data has made it difficult to track who is receiving the help. The report’s authors urge the bank to practice more-transparent reporting practices that include race, ZIP code, and income data for all foreclosures, short sales, and principal reductions.

According to Adams, the data for relief efforts and other information is available through industry publications such as RealtyTrac and Inside Mortgage Finance, as well as government sources.

Last year, the bank settled a lawsuit with the Justice Department, which alleged that the financial institution had discriminated against minority borrowers during the housing bubble, charging higher fees and rates to minorities than whites, even when they had the same credit risk.

The Wells Fargo case wasn’t unique: Lawsuits surrounding discriminatory housing practices and predatory sub-prime mortgage lending hit major banks everywhere.

(RELATED: Big Banks, Racial Discrimination Linked in Housing Crisis)

Using data from the Home Mortgage Disclosure Act Database, the report found that between 2007 and 2009, Wells Fargo was 188 percent more likely to put African-Americans into riskier sub-prime loans than white borrowers with similar credit history; the risk for Hispanics was 117 percent.

Adams maintains that Wells Fargo is a “fair and responsible lender” that adheres to regulations according to the Fair Lending Act. She added that the bank works closely with various advocacy and real estate organizations to help minority and low-income borrowers.

The report, co-authored by the Alliance of Californians for Community Empowerment, Center for Popular Democracy, and the Home Defenders League, asks Wells Fargo to commit to principal reductions in the interest of saving homeowners from complete financial ruin.

Between 2009 and 2012, Wells Fargo granted $6.3 billion in principal forgiveness; their goal is to hit $7 billion by 2014, Adams said.

“We take it very seriously, and we work very hard at it. We really are focused on excellence, helping our customers succeed financially, and we have a culture of continuously improving our home-lending activity,” Adams said.

The report argues that allowing all 65,466 homes in California to be foreclosed would be a detriment to the state and local economy. Foreclosure would cause the homes to lose 22 percent of their value, at an estimated cost of $7.6 billion. Maintenance costs for vacant homes would cost the government $19,227, resulting in a total cost of nearly $467 million for taxpayers.

“Communities have already sustained significant harm from the foreclosure crisis; unless Wells Fargo changes its practices, more harm will be done in coming months and years. New homes continue to enter the pipeline, inflicting tremendous stress and damage on homeowners and communities until Wells Fargo adopts significant new policies,” the report states.

Source

For immigrants fighting deportation, a push for government-funded lawyers

For immigrants fighting deportation, a push for government-funded lawyers

Nearly 4,000 immigrants in the Washington region face deportation every year without a lawyer, according to a report that calls on area governments to follow the lead of New...

Nearly 4,000 immigrants in the Washington region face deportation every year without a lawyer, according to a report that calls on area governments to follow the lead of New York and Los Angeles and provide funding for legal aid to immigrants.

The Center for Popular Democracy, a national nonprofit organization, analyzed thousands of deportation cases at immigration courts in Baltimore and Arlington and found that immigrants were far more likely to prevail if they had a lawyer...

Read full article here.

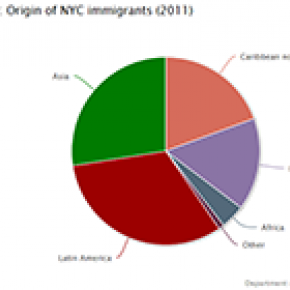

City Municipal ID Cards Could Boost Immigrant Business

Crain's New York Business - July 8, 2014, by Chris Bragg - An initiative creating an identification card for New York City residents could allow hundreds of thousands of undocumented immigrants to...

Crain's New York Business - July 8, 2014, by Chris Bragg - An initiative creating an identification card for New York City residents could allow hundreds of thousands of undocumented immigrants to open bank accounts, where identification is required. That is just one way the law could boost the city's economy, according to advocates for the card, though thorny security concerns for the city remain unresolved.

Aimed at making life easier for the city's half-million undocumented immigrants, the bill to create a municipal identification card was passed by the City Council last month, and Mayor Bill de Blasio is expected to sign it. A secondary impact could be boosting immigrants' spending and entrepreneurship, say advocates.

"The multiplier effect of the municipal ID is going to be huge because of the financial empowerment aspect," said Steven Choi, executive director of the New York Immigration Coalition. "People who don't have IDs or a bank account can't participate in the financial system."

Applicants for the cards, which the city is expected to begin issuing in late 2014 or early 2015, will have to prove their identities with birth certificates or passports from any country. They will also have to prove their city residency with documents such as utility bills or pay stubs.

The cards will include a person's name, picture, address and date of birth. But questions remain whether that will be enough for banks, which have security concerns and have not yet publicly committed to accepting the IDs. For one, undocumented immigrants do not have Social Security numbers.

Mr. Choi believes these immigrants could apply for Individual Taxpayer Identification Numbers (ITINs), a tax-processing number for which foreign workers can apply. Banks currently have inconsistent polices on whether to accept ITINs in lieu of Social Security numbers, but Mr. Choi thinks that having the city government's full weight behind the initiative will prod the institutions to accept them.

Banks have concerns about the cards being secure enough, and fear that accounts could be used for money laundering. Whether or not banks large and small decide to accept the ID cards will likely rest on the Federal Deposit Insurance Corp. and state Department of Financial Services giving their sign-offs, according to Brian Blake, vice president of Spring Bank, a community lender that focuses primarily on low-income and underserved neighborhoods.

"There are a lot of banks that have flexibility above the minimum requirements to open an account, and below that minimum there's no flexibility," Mr. Blake said. "We try to be as open-minded as possible, as far as the regulators allow."

Although the City Council overwhelmingly passed the bill, the measure faced opposition from the chamber's three Republican members, who cited security concerns. Republicans in Albany are set to make the cards a campaign issue in the 2014 election, saying they legitimize immigrants who are here illegally and create the potential for fraud and abuse.

Another key question is whether a broad swath of New Yorkers—not just undocumented immigrants—will apply for the municipal ID cards. Advocates say that for immigrants to avoid being stigmatized, card ownership must extend beyond those living here illegally.

To that end, the city is planning on putting benefits such as discounts to museums on the cards.

That could encourage a whole new population to take in New York's cultural institutions—including both undocumented immigrants and citizens—although the details have yet to be worked out. Cities that have passed municipal ID laws, such as San Francisco, Los Angeles and New Haven, Conn., have employed these incentives.

Signing leasesThe cards are also intended to ease holders' abilities to sign leases and give them access to government buildings, which often require identification, said Andrew Friedman, co-executive director of the Center for Popular Democracy, a New York-based group that released a study on the impact of similar laws around the country.

That could make it easier for entrepreneurial immigrants to deal with regulators and other gatekeepers of the area's economy.

"For immigrant-owned small businesses and vendors seeking to open and get a license, it makes a huge difference," Mr. Friedman said.

Source

Puerto Rico Activists Crash Federal Reserve Panel With Creative Protest

Puerto Rico Activists Crash Federal Reserve Panel With Creative Protest

NEW YORK — Over a dozen activists descended on a building where Federal Reserve chair Janet Yellen and her three living predecessors were speaking on Thursday to demand that the Fed bail out...

NEW YORK — Over a dozen activists descended on a building where Federal Reserve chair Janet Yellen and her three living predecessors were speaking on Thursday to demand that the Fed bail out Puerto Rico’s cash-strapped government.

The demonstrators, who are affiliated with the progressive Fed Up coalition, distributed Puerto Rican flags and empanadas as Puerto Rican music played outside Manhattan’s International House, a student residence. Yellen was there for an unprecedented panel discussion alongside past Fed chairs Ben Bernanke, Paul Volcker and Alan Greenspan, who participated via videostream.

The activists were joined by Puerto Rican lawmaker Manuel Natal, who was in town to participate in a panel discussion hosted by City Council Speaker Melissa Mark-Viverito on Friday.

“They have two mechanisms under their authority to help Puerto Rico: one is to provide a bailout to Puerto Rico similar to the one they did to banks, the same banks that are now in Puerto Rico making a fortune out of our fiscal situation,” Natal said. “And the second would be to buy our debt” and charge Puerto Rico interest rates that are lower than the market would offer.

The activists claim that since the Fed had the authority to buy trillions of dollars of bad debt from Wall Street banks after the 2008 financial crisis, it can do the same for the debt of Puerto Rico.

Economic observers with knowledge of the Fed’s functions consider that argument dubious. Joseph Gagnon, a senior fellow at the Peterson Institute for International Economics who was an economist at the Fed Board of Governors for many years, said that the Fed is not allowed to buy municipal debt — of the kind Puerto Rico owes — that comes due over a period longer than six months. He also said such a purchase would be inconsistent with the Fed’s dual mandate of maintaining price stability and full employment.

The Fed has “never bailed out any insolvent entity as far as I know. They always demand collateral sufficient to cover any loan,” Gagnon said, as the Fed did when it provided aid to major U.S. banks.

Natal, the lawmaker, also believes some of Puerto Rico’s debt has been issued unconstitutionally and can therefore be nullified.

Greg Williams, a spokesman for Jubilee USA, a coalition of faith-based groups that advocates for global debt relief policies, declined to endorse a Fed bailout, but suggested the Fed could broker a deal instead.

“We support a proposal where the Fed facilitates a restructuring process,” Williams said.

More important than the details of the demonstrators’ demands, however, is the protest’s political symbolism in the midst of a heated battle over Puerto Rico’s future. The demonstration was perhaps the most colorful in a series of political moves and counter-moves by the Puerto Rican government and its sympathizers on one hand and the commonwealth’s bondholders and their allies on the other. Both seek to influence a congressional rescue plan that could enable Puerto Rico to restructure its debts.

Members of Congress from both parties are negotiating changes to the draft of a relief bill released last week by the House Committee on Natural Resources, which has jurisdiction over U.S. territories.

But many in Puerto Rico, and some progressives in the mainland United States, object to the Washington-based federal oversight board the bill would introduce to audit Puerto Rico’s finances and recommend reforms. Under the terms of the bill, Puerto Rico would pursue voluntary compromises with its creditors; failing that, the board could greenlight court-supervised debt restructuring that would force bondholders to accept the losses.

Those critics of the draft bill — including lawmaker Natal — view the board as having the trappings of American colonial rule over Puerto Rico.

Critics of the draft House bill say it has the trappings of American colonial rule over Puerto Rico.

They also argue that Puerto Rico should not have to meet any conditions to gain access to court-supervised debt restructuring. Puerto Rico, unlike the fifty mainland states, lacks the power to grant its municipalities and public corporations federal bankruptcy protections.

Puerto Rico is taking a multi-pronged approach to secure debt relief that appears designed to increase its leverage with creditors and win terms that are as favorable as possible.

The island’s governor, Alejandro Garcia Padilla, signed a bill on Wednesday that would empower him to declare a state of emergency and enact a moratorium on the island’s $70 billion debt. Puerto Rico’s next major debt payment — a $422 million tranche — comes due on May 1.

Daniel Hanson, a Puerto Rico specialist for the financial analysis firm The Height, wrote in an email newsletter that Puerto Rico’s creditors will likely challenge the moratorium in court, where Puerto Rico’s “playbook is not likely to be persuasive to American courts adjudicating the contracted rights of creditors.”

Garcia Padilla has said the island is incapable of paying its debts in full. Puerto Rico has enacted spending cuts and tax hikes in recent years that have stifled its economy and depleted its social services, creating a situation that many people already characterize as a humanitarian crisis.

Puerto Rico also argued for the right to enforce a local bankruptcy law that went before the Supreme Court last month after lower courts had blocked the island from putting it into effect. The high court is expected to rule in the case by late June.

In Congress, Democrats sensitive to Puerto Rico’s plight — and solicitous of the votes of former island residents living on the mainland — hope to dilute some of the proposed oversight board’s sweeping powers.

The Height’s Hanson, however, expects subsequent iterations of the House bill to be “more creditor-friendly,” he wrote.

Meanwhile, organizations representing Puerto Rico’s powerful creditors have stepped up their efforts to amend the legislation to limit the restructuring authority that the island would get. The commonwealth’s bondholders include a significant number of so-called vulture funds, which are hedge funds that have bought its debt from other creditors at discounted rates on the promise of recovering the obligations’ original full-dollar value.

A group called Main Street Bondholders, which claims to represent ordinary retirees, has created a web site attacking the draft House bill for granting Puerto Rico “super Chapter 9” bankruptcy protections.

Main Street Bondholders is associated with the conservative seniors group 60 Plus, which played an active role in the fight against the Affordable Care Act. The New York Times reported in December that 60 Plus is funded by a handful of large, anonymous donors and was recruited into the effort by a Republican public relations firm that also represents BlueMountain Capital, a creditor that has been outspoken against federal government help for the island.

The fight over whether to help Puerto Rico has reached the bottom rung of American discourse — cable news ads paid for by undisclosed donors. The ad, which ran on CNN and was paid for by the Center for Individual Freedom, urges Congress to “stop the Washington bailout of Puerto Rico.” The Virginia-based conservative group does not disclose its donors. It was founded in 1998 to combat government restrictions on smoking.

The CFIF did not respond to a Huffington Post question about whether any of its funders have a financial stake in the outcome of the Puerto Rico bailout.

By Daniel Marans & Ben Walsh

Source

Puerto Rico: "No te hemos olvidado"

La semana pasada marcó dos meses desde la devastación del huracán María en la bella isla de Puerto Rico. A pesar de todo este tiempo, más de la mitad de la isla -más de un millón de personas- aún...

La semana pasada marcó dos meses desde la devastación del huracán María en la bella isla de Puerto Rico. A pesar de todo este tiempo, más de la mitad de la isla -más de un millón de personas- aún están sin electricidad, las enfermedades propagándose y muchos aún no tienen los recursos necesarios para reconstruir sus hogares y sus vidas.

Lea el artículo completo aquí.

2 months ago

2 months ago